Petronet LNG, India – A business analysis

First analysis - 16th Dec 2023

Background

As of 2023, Petronet is a simple business. It has two, port-based LNG regasification terminals in Dahej and Kochi, with current capacities of 17.5 and 5 MMTPA respectively. Petronet has long-term contracts with several suppliers like Qatar (7.5MMTPA) and MARC (1.425 MMTPA – an Exxon branch), as well long-term contracts with customers like IOCL, BPCL, GAIL etc. (8.25MMTPA). This part of the business is like a utility business and is not sensitive to LNG prices, since it is pass through at (pre)negotiated rates. A smaller part of the business also buys LNG on the international spot market and sells it to customers, like the fertilizer industry, that are price sensitive and will swap LNG for alternative fuels like coal if LNG is too pricey. This part of the business is like a commodity business and carries inventory risk.

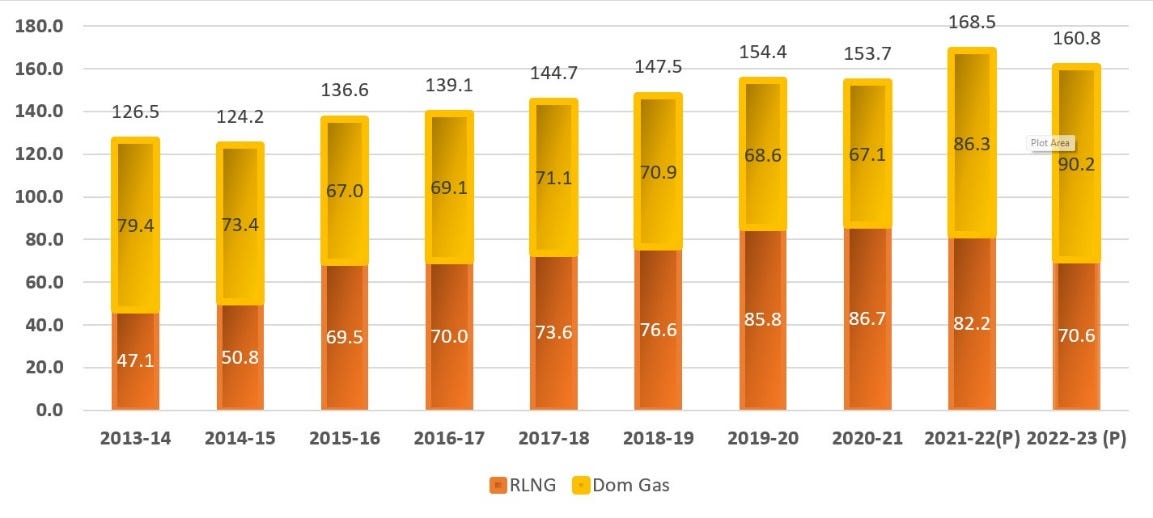

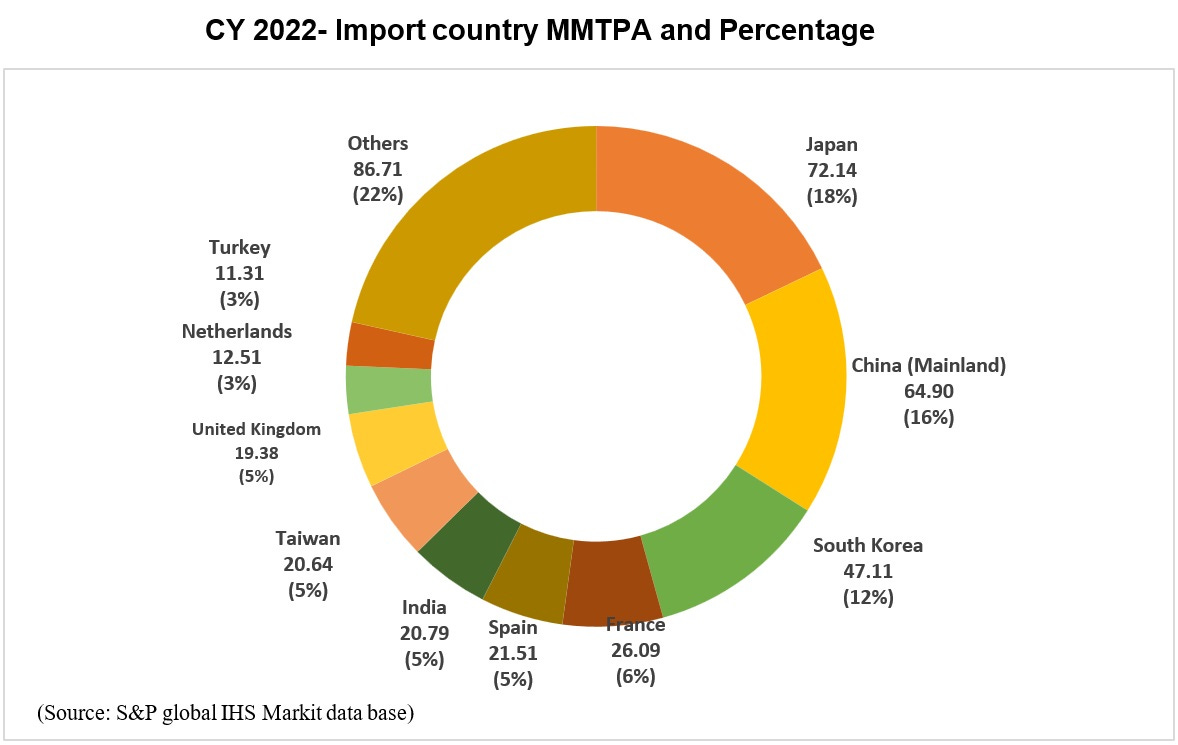

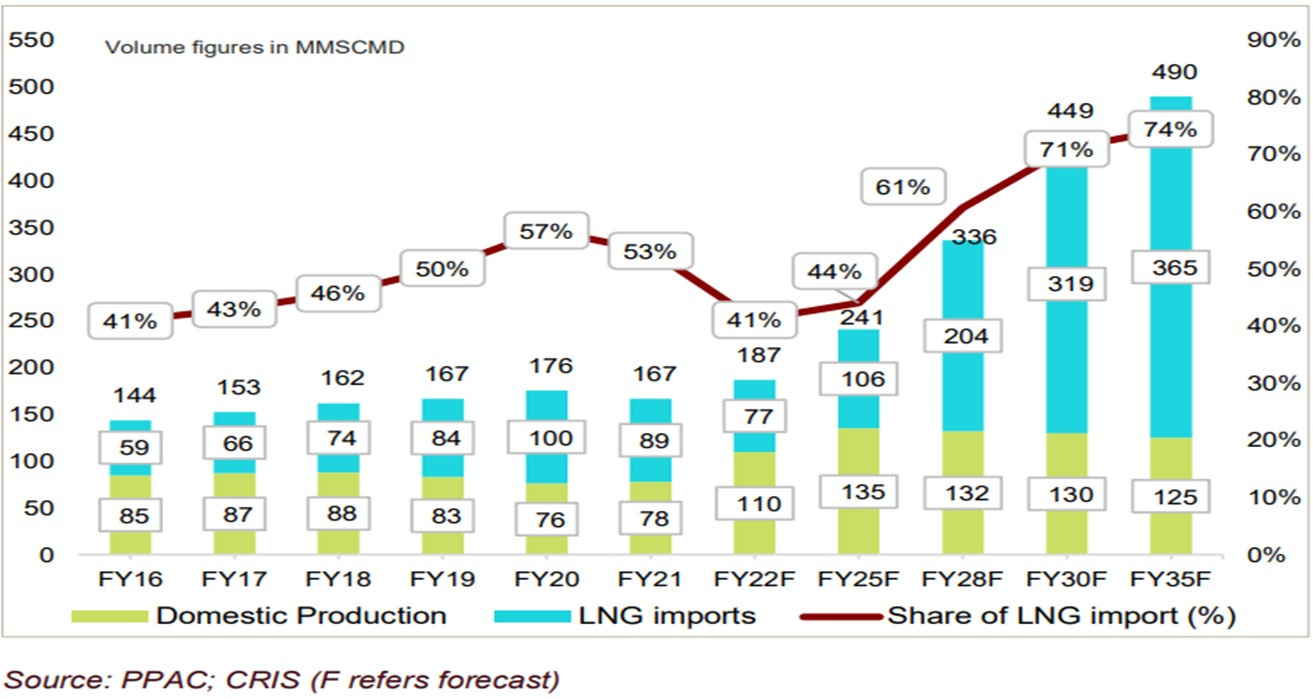

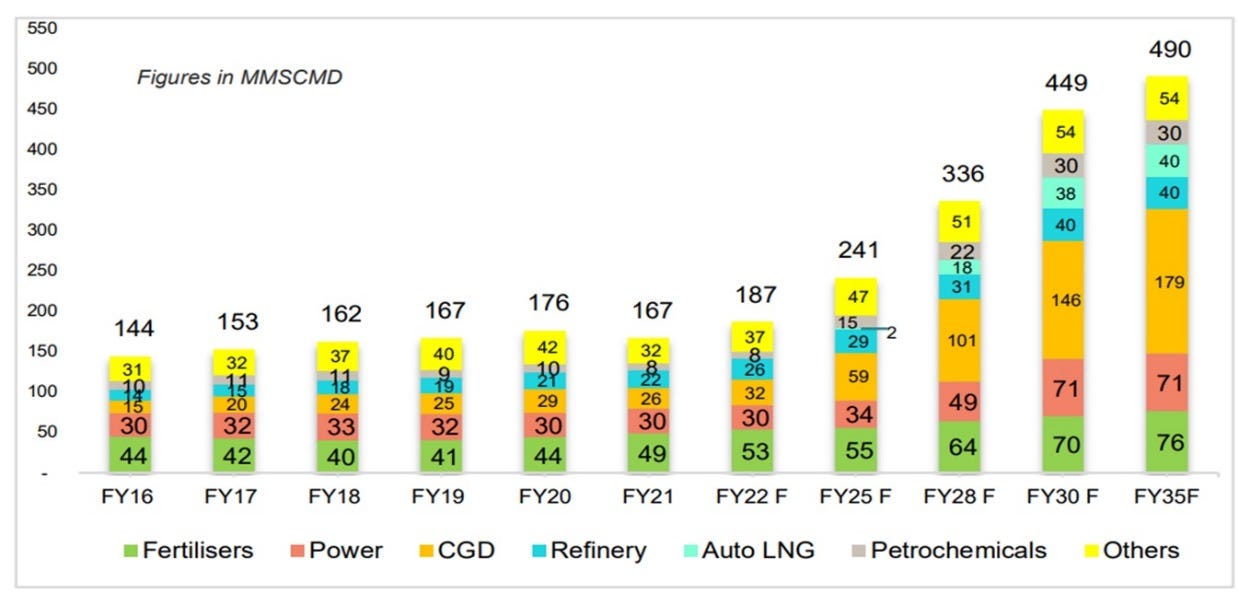

In the CY 2022, India had long term LNG contracts of almost 20 MMTPA, which constitutes approximately 95% of around 21 MMTPA LNG consumption (Annual Report 2023). Since India is a gas deficit country and relies heavily on LNG imports, Regasification Terminals play an important role in the country’s gas development plans. The share of LNG in India’s gas consumption stood at around 44% in the FY 2022-23. See Figure 1, Figure 2 Figure 3 for more details.

Figure 1: Gas consumption in MMSCMPD (to convert to MMTPA, divide by 3.6).

Figure 2: LNG imports by different countries.

Figure 3: LNG as percentage of expected gas consumption in India.

Current regasification capacity in India is 47.7 MMTPA. Only Petronet’s LNG terminal at Dahej and Shell’s terminal at Hazira are operating at near optimal capacity. Other terminals remain underutilized and operate at less than 25% of their regasification capacity. 17.5 MMTPA of the 21MMTPA of pan-India imports were at Dahej. Figure 4 gives details.

Terminals at Kochi and Ennore are operating below capacity due to insufficient pipeline connectivity with the demand centers. The 5 MMTPA Dabhol terminal is being operated at low capacity owing to the absence of breakwater required for protecting LNG ships during the monsoon season (https://www.henergy.com/lng-ngii).

Figure 4: Capacity utilization at various LNG terminals.

There are new Regasification projects under construction by different companies at various locations namely Jaigarh, Jafrabad, Chhara and Petronet’s greenfield floating stage regasification unit based LNG terminal at Gopalpur on East Coast along with expansion of Petronet’s existing regasification terminal at Dahej from 17.5 MMTPA to 22.5 MMTPA. It is expected that with the completion of all these new terminals and expansion projects, the total regasification capacity in India will increase from 47.7 MMTPA to 72.7 MMTPA.

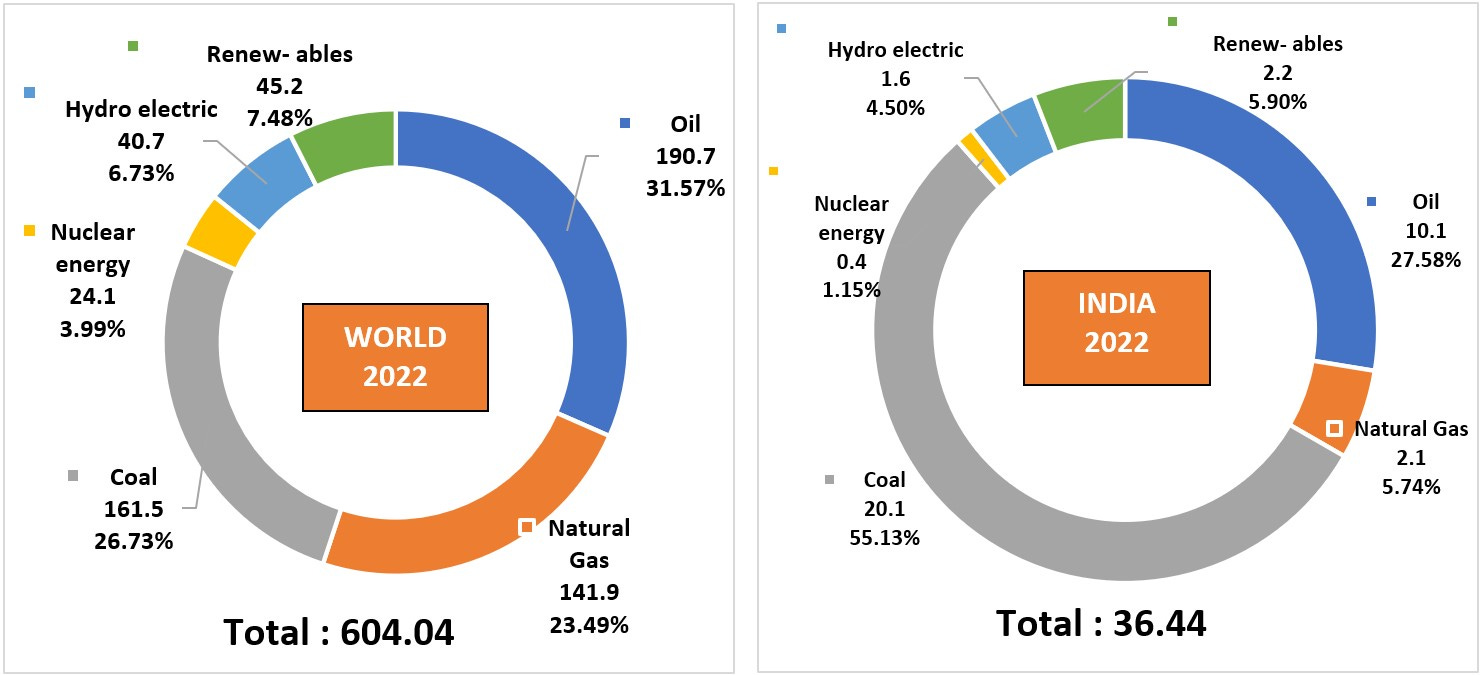

In order to achieve 15% share of Natural Gas in the energy basket of India by the year 2030 (from 6.2% at present, see Figure 5), India would require around 150 MMTPA of LNG re-gas infrastructure. Thus, creating additional capacity of over 77 MMTPA is necessary. The drivers of increased gas demand are shown in Figure 6.

Figure 5: Energy consumption mix by world versus India.

Figure 6: Drivers of gas consumption by industry.

Since domestic capacity is limited, growth in gas consumption can only be met through importing LNG unless there are piped gas connections to India, e.g., underwater piped gas from the middle east to the western seaboard. Such a project, however, takes decades to conceive and develop.

Business drivers

While the regasification capacity of India is more than 2 times the current imported volumes of LNG, the Dahej terminal alone is responsible for 80% of pan-Indian imports. Dahej is the crown asset of Petronet because of the dense network of gas-pipelines that connect to Dahej and its proximity of the middle-east. See Figure 7! While terminal run by other companies will slowly get connected to the gas network, its going to be a long and unpredictable process. With secular demand for increased LNG, that’s not going to be a problem for Dahej.

Also, Dahej’s capacity is increasing from 17.5 to 22.5 MMTPA with 2.5MMTPA increase expected by 2024. The pipeline between Kochi and Bangalore has continuously had challenges, in the coming years it will get completed (thus integrating into the national gas grid) leading to a huge increase in the capacity utilization from 20-30% to 80%. So effectively, for Petronet, its gas-pipeline connected capacity will go from 17.5 to 27.5 MMTPA (60% increase). Keep in the mind that the pipelines are not owned or maintained by Petronet, thus no maintenance capex related to these. That’s why, Petronet has a high ROE and ROCE, 26 and 22% respectively.

Figure 7: Map of gas pipelines in India (2021). Source here

Analysis of Financial Statements

From a balance sheet standpoint, there is no debt – in fact the market cap is INR 321,000 million while the TEV is 270,000 million, so nearly 5000 million in cash on the balance sheet. Book value is nearly 50% of the market cap (150,000 million).

From an income statement perspective, revenue and EPS growth is 14% and 10% respectively over the last 5 years (Table 1). These should expand considerably as new capacity becomes available in the coming years. A dividend yield of 3.3% that grows regularly is also decent.

In 2023 FCF was lowered because of capacity expansion and the building of a 3rd Jetty at Dahej – no worries, a good use of capital!

Table 1: Key metrics from financial statements in millions INR over the past five years.

Under average 5-year FCF assumptions and modest growth rates, Petronet seems like a decent investment with returns of 10-12 percent with limited downside. FCF should increase with a nearly 60% increase in planned capacity that is almost guaranteed to come online in the next years.

Table 2: A DCF valuation for normal, best case and worst-case scenarios using FCF as input.

Investment thesis

With a strong balance sheet, good ROIC and excellent gas pipeline connectivity to its terminals, Petronet is a predictable business that produces reliable FCF – these might vary year-to-year based on new contracts being negotiated and the ongoing spot market rates, but over a few years, things will even out. With secular demand for increased gas use, importing LNG is unavoidable. Petronet gets a piece of the pie, come what may. Just keep in mind that one of the risks is that Petronet is still a government company.

Company news

Petronet on 31st Oct 2023 announced a greenfield expansion into petrochemicals at Dahej – an entirely different business and likely deworsification. The proposed project includes a 750 KTPA of Propane Dehydrogenation (PDH) & a 500 KTPA of Propylene (PP) plant including propane and ethane handling facility. The cost will be INR 210,000 Million and will take 4 years for development. The cost per se is not an issue – it can be covered by the upcoming 4 years of FCF and the cash on the balance sheet. Of course, taking some debt will not be a problem either. In effect we will be transferring FCF for the next 4 years into equity. The question to ask is what will the ROE be on the invested capital? I assume, the project will take about 7 years – 4+ years for development and then a year+ for the factory to get fully operational. So, worst case, we are going to see cash flow from this development only from 2030. I expect ROIC for Petronet to get to and stay in the low teens for the next years and no meaningful change in stock price. Here’s a report by Emkay on Petronet’s petrochem foray.

Catalyst

I like the regasification business and at current prices would be willing to buy it. But the foray into Petrochem means that FCF of next years will disappear and ROE on this investment is not visible. If price falls by 25% to around INR 150 per share, then wake me up as that would give some margin of safety!